Hormuz: Security Risk Reprices Transit Capacity

When military engagement meets chokepoint vulnerability, throughput contracts before supply disappears

Key Takeaways

Transit through the Strait of Hormuz continues at sharply reduced levels, with only limited shipments proceeding under current conditions.

The waterway remains physically open, but usable capacity is constrained by elevated security conditions affecting routine operations.

Carrier participation is declining as operators delay, reroute, or avoid transits under current threat and cost conditions.

Insurance coverage is becoming more restricted and expensive, limiting access required for standard commercial shipping activity.

Escort availability is capping transit volume, concentrating movement in prioritized cargoes and state-backed shipments.

Iranian forces attacked U.S. naval assets in the Strait of Hormuz using missiles, drones, and small boats, after which U.S. Central Command conducted retaliatory strikes on Iranian military and maritime targets in the same area. No U.S. destroyers were hit, while Iran claims civilian damage. Commercial shipping through the strait has sharply declined, with only limited, exceptional transits, and oil prices have risen above prior levels.

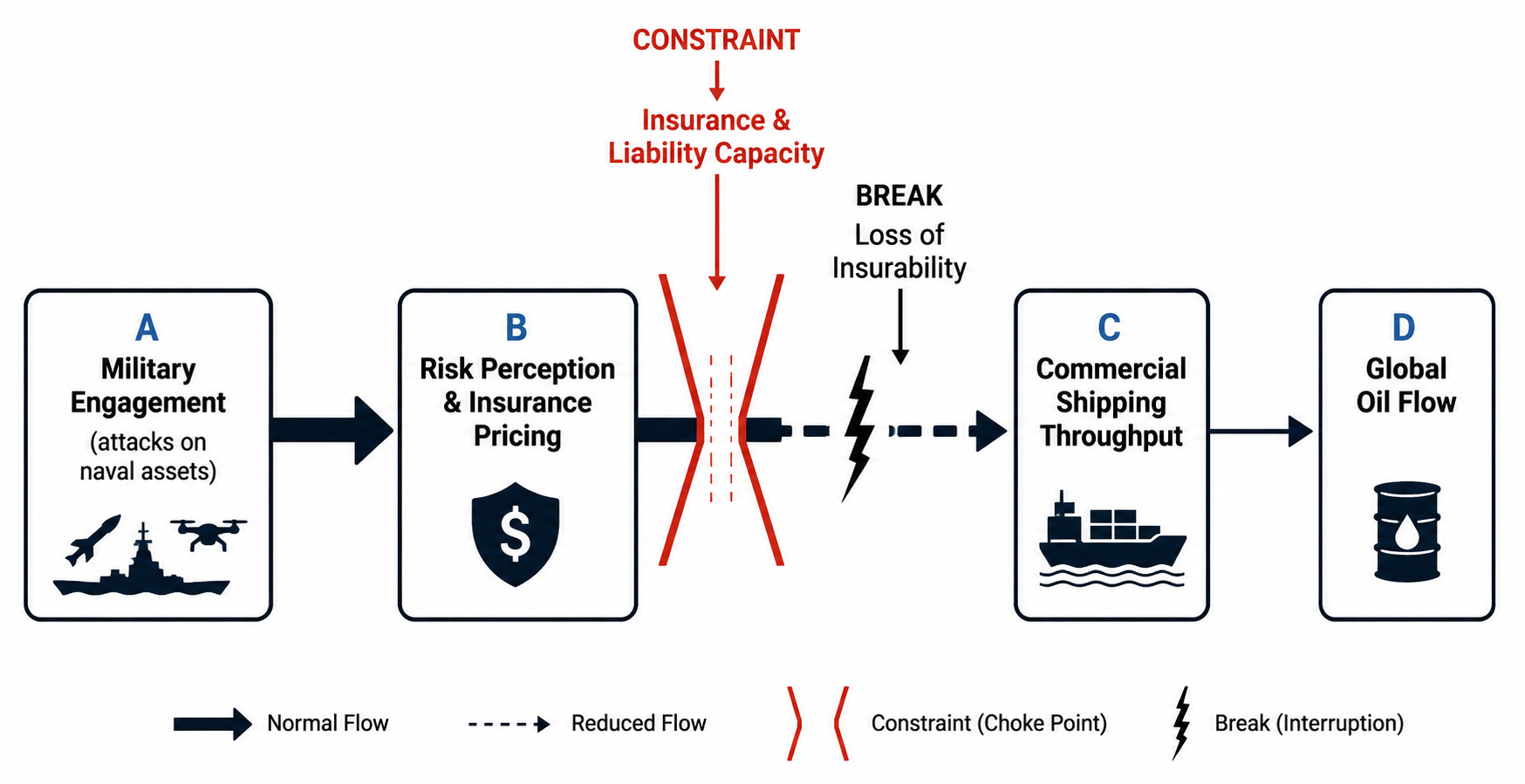

The constraint is not physical closure but security-dependent throughput. The strait remains open in principle, yet usable capacity collapses as risk rises. Transit becomes conditional on survivability rather than navigability. This converts a geographic chokepoint into a probabilistic filter: passage exists, but not at scale.

The mechanism operates through risk pricing and coordination breakdown. Attacks on naval assets degrade confidence in escort reliability and ceasefire credibility. Insurers raise premiums or withdraw coverage, shipowners delay or reroute, and escorts cannot scale fast enough to restore confidence. Throughput falls before supply is exhausted because coordination fails under elevated risk.

Opposing forces attempt to stabilize flow. Military escorts, signaling restraint, and selective routing aim to preserve minimal transit. Producers with alternative export routes or storage buffer the shock. Importers draw on inventories. These actions slow contraction but do not remove the constraint; they redistribute exposure across actors.

The external bottleneck is insurance and liability capacity. Even if naval presence increases, without insurable conditions, commercial actors cannot operate at scale. Financial intermediation, not physical passage, becomes the limiting factor. As premiums and uncertainty rise, marginal voyages drop out first, compressing total flow.

Stabilization would require credible deconfliction that lowers perceived risk enough to normalize insurance and restore routine routing. Absent that, the system equilibrates at a lower throughput where only high-margin or state-backed shipments move.

A sustained, verifiable restoration of escorted commercial transit with normalized insurance pricing would break this claim.

Pathways: When military escalation meets chokepoint dependency, supply continuity fragments along security gradients

In the coming months, traffic remains intermittent as insurers reprice risk and carriers avoid unescorted passages, creating a throughput bottleneck defined by convoy availability rather than channel width. The U.S. Navy and allied forces ration escort capacity, prioritizing strategic cargoes, while Gulf exporters draw down storage to smooth deliveries. The switching cost of rerouting—limited pipeline alternatives and contractual obligations—locks flows into partial utilization of Hormuz despite elevated risk. A failure point appears if coordinated naval deconfliction restores predictable corridors, collapsing premiums and re-expanding transit faster than escorts can scale.

Over the next one to two years, producers and importers reconfigure around persistent insecurity: incremental pipeline expansions bypassing the strait, long-term contracts embedding risk surcharges, and refinery optimization toward more flexible crude slates. The constraint shifts from immediate passage risk to capital allocation under uncertainty, with a bottleneck in financing projects whose payoff depends on the durability of disruption. National oil companies and large traders absorb volatility through balance sheets, while smaller shippers exit or consolidate, raising concentration. The lock-in emerges through sunk infrastructure and contract structures that favor established routes even as alternatives become marginally viable. The constraint loosens if insurance markets normalize on the back of sustained incident-free periods, undercutting the economics of bypass capacity.

Over a longer horizon, the mechanism itself evolves: energy systems reduce exposure to a single maritime chokepoint through diversification—LNG routing flexibility, electrification at the margin, and regional supply loops—shifting the constraint from a geographic passage to system-wide coordination and storage. The bottleneck becomes grid integration and storage capacity rather than tanker lanes, with high switching costs embedded in legacy refining and transport assets. Major importers institutionalize strategic reserves and demand-response mechanisms as standard buffers, while exporters diversify customer bases and delivery modes. The constraint ceases to bind if alternative systems reach sufficient scale to decouple price formation from Hormuz transit conditions.

Which path dominates depends on whether security risk in the strait is episodic or structurally persistent, and whether financial and institutional responses treat it as a temporary shock or a durable condition shaping investment.

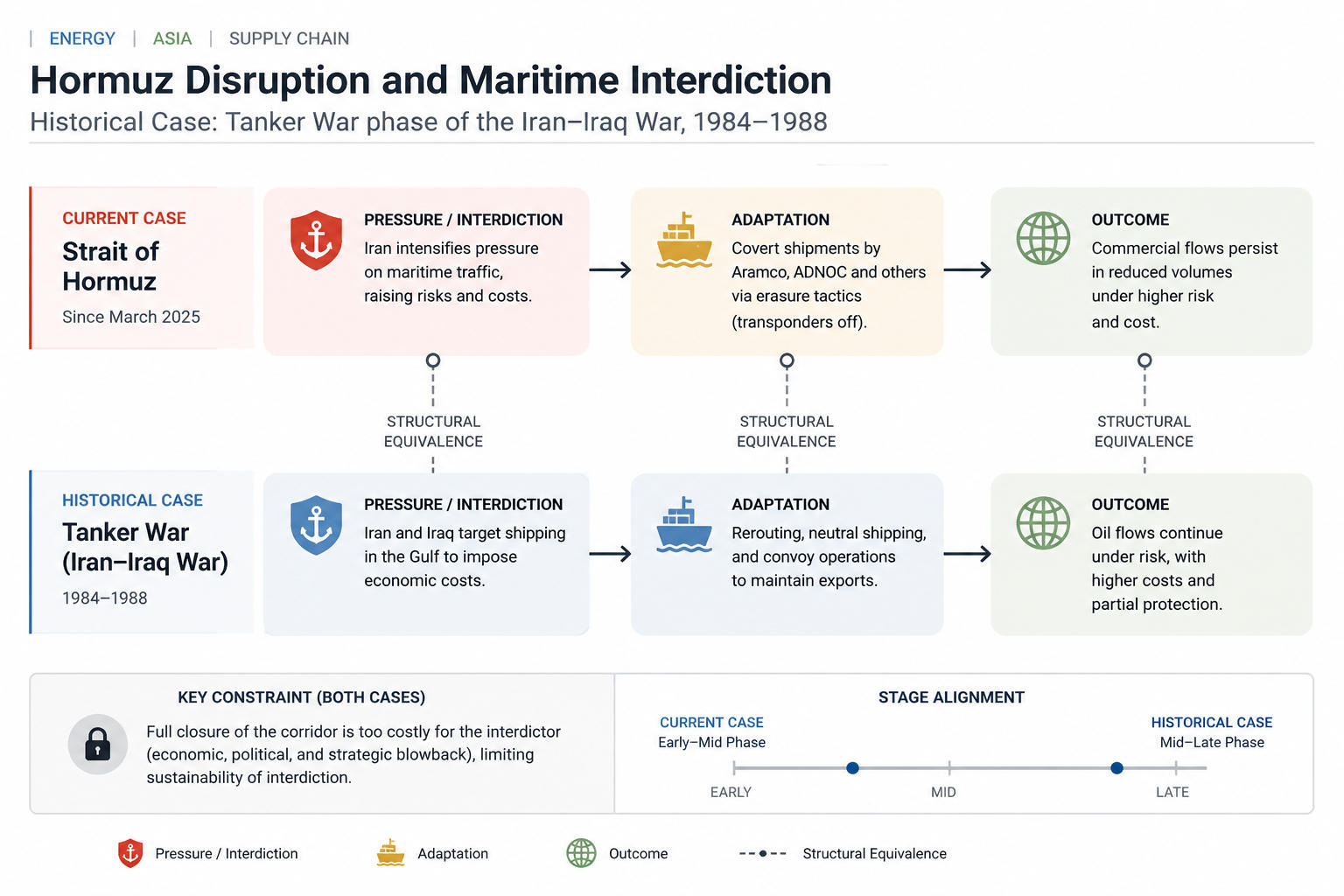

Historical precedent: Tanker War (Iran–Iraq War, 1984–1988)

Iranian forces striking U.S. naval assets and U.S. retaliatory actions compress the Strait of Hormuz into a security-constrained passage, where transit becomes conditional rather than routine. The tension sits between military signaling/control and the continuity of commercial energy flows, forcing a comparison to prior episodes where conflict pressure bound a maritime chokepoint.

In both the current case and the Tanker War phase of the Iran–Iraq conflict, attacks on shipping and naval assets increase perceived and priced risk, which transmits directly into reduced tanker movement. The mechanism aligns: targeted disruption → elevated insurance and threat environment → voluntary or forced reduction in commercial transit → constrained throughput of energy exports. Opposing forces are structurally equivalent: actors applying pressure through maritime insecurity versus actors attempting to maintain flow through protection, rerouting, or risk absorption.

The current situation is in an early-to-mid phase relative to the Tanker War’s escalation cycle, where attacks are present but not yet systemically saturating all traffic. In the historical case, the mid-to-late phase saw widespread targeting, reflagging operations, and sustained naval escort systems as necessary countermeasures. The binding constraint in both cases is identical: throughput capacity is not physically destroyed but functionally reduced by security risk, with insurance costs, escort availability, and threat density acting as the operative bottlenecks.

The analogy weakens where external naval dominance and global energy system flexibility differ: the present configuration includes broader international naval capacity and more diversified supply routes than during the 1980s, altering both the ceiling of disruption and the pathways of adaptation without removing the underlying constraint.

Flow does not stop when attacked; it thins until risk is priced out.